How to Overcome the Complexity of Central Bank Digital Currency Systems with Quality Engineering

We explore the critical role of quality engineering in the successful implementation of Central Bank Digital Currency (CBDC) systems. Discover how meticulous quality control and testing processes are pivotal in building trust and resilience within the CBDC ecosystem and ever-evolving financial landscape.

Rakesh Reddy Lokireddy, COE Leader, Blockchain

Sep 15, 2023

7 min read

Get a free maturity assessment for your organization.START NOW

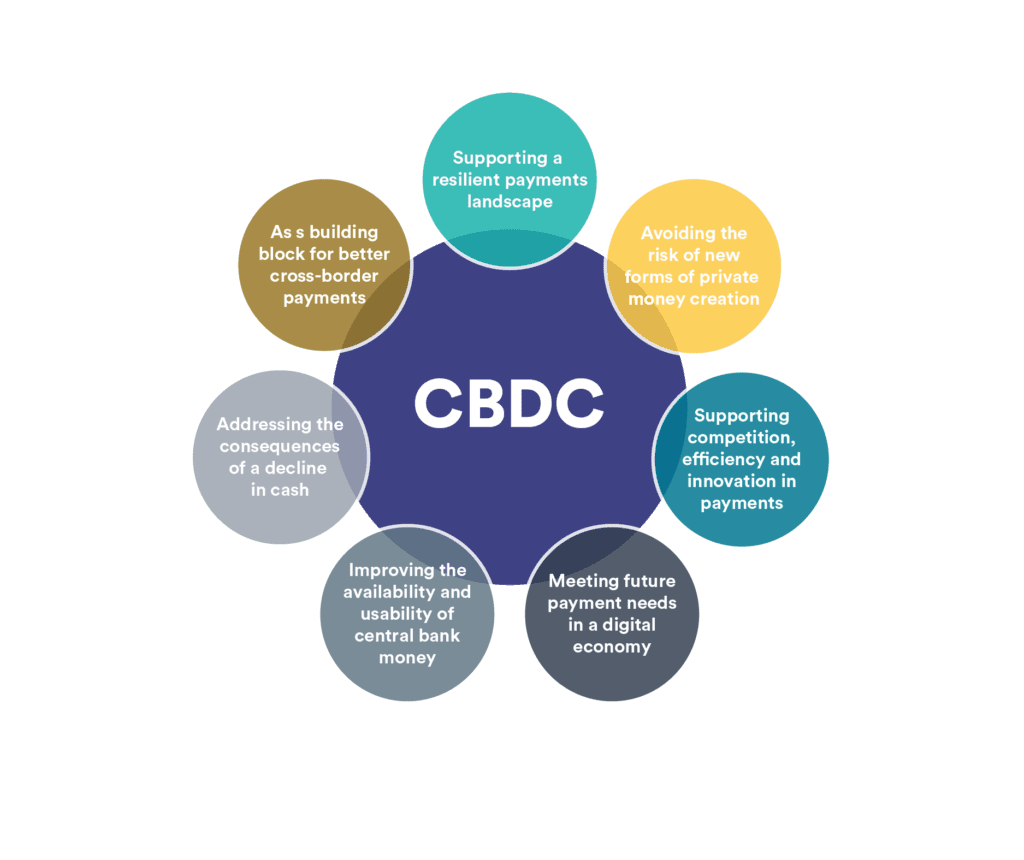

Central Bank Digital Currency (CBDC) is a digital form of a country’s official currency. To properly understand CBDC, it’s helpful to contextualize its distinct difference from other digital assets.

What is a digital asset?

Digital asset refers to a wide range of digital or blockchain-based tokens or cryptocurrencies, such as Bitcoin or Ethereum. These assets are typically decentralized technologies and are not issued or controlled by a central authority. They are often used for investment, speculation, and as a means of transferring value across borders without intermediaries.

What is CBDC?

CBDC, on the other hand, is a digital form of an official sovereign currency (e.g. the US dollar or the Euro) issued and regulated by the central bank or government. CBDC is designed to function as a digital representation of physical currency, and it aims to provide a secure and efficient means of payment while retaining the stability and trust associated with traditional fiat currencies.

The emergence of CBDC

The Banking International Settlements (BIS) survey report discloses that CBDCs are being investigated by nine out of ten central banks, and more than half are now creating or conducting actual trials with them. In particular, the development of retail CBDCs has advanced.

According to the IMF, “We know that the move towards CBDCs is gaining momentum, driven by the ingenuity of central banks. All told, around 100 countries are exploring CBDCs at one level or another. Some researching, some testing, and a few already distributing CBDC to the public.”

CBDC architectural models

CBDCs can be implemented using various architectural models, each with its own characteristics and implications. Here are some key CBDC architectural models:

Direct CBDC

In this model, central banks have exclusive control over CBDC operations, including issuance, transactions, user interactions, and ledger management. The key advantage is the public’s trust in central banks, enhancing CBDC credibility and easing concerns about its relationship with traditional currency.

Indirect CBDC

Similar to our current payment system, commercial banks oversee transactions with central bank money, while the central bank doesn’t retain transaction records. Intermediaries manage indirect CBDCs, handling communication with retail clients and sending payment messages to other intermediaries and central banks for wholesale payments.

Hybrid CBDC

In this model, the central bank issues the CBDC but allows for private firms to take on an intermediary role. This entails the onboarding of end users, asserting that private actors such as deposit taking institutions or payment providers have a competitive advantage in this area. Here private actors would also play a role in managing retail payments effectuated in CBDC. Central banks would keep full retail records of all CBDC balances. This would enable them to react to any failure by private payment managers and to safeguard the business continuity of the CBDC payment process.

CBDC use cases

Central Bank Digital Currencies (CBDCs) offer diverse applications across sectors. Common use cases include:

Retail Payments

CBDCs replace cash and traditional methods, enabling swift, secure digital transactions for goods and services. Technologies like DLT or blockchain streamline transactions for in-store and online shopping.

Cross-Border Payments

CBDCs simplify international transfers, reducing fees, processing times, and enhancing remittances and trade for banks and capital markets. Notably, BIS lists 5 CBDC projects: Dunbar, Jura, mBridge, Mariana, and Icebreaker.

Smart Contracts

CBDCs integrate with smart contracts for automated, IoT-driven payments. For instance, EVs can autonomously pay for charging services via CBDC, ensuring seamless, efficient transactions.

Peer-to-Peer Transactions

CBDCs enable real-time peer-to-peer transactions, eliminating intermediaries. RBI’s e-rupee pilot explores P2P and P2M transactions via QR codes.

Emergency Fund Disbursement

CBDCs aid efficient government assistance during disasters, ensuring swift, traceable fund distribution to affected individuals.

CBDC technology layers

The implementation of CBDC involves several technology layers that work together to create a functional and secure digital currency system. The primary technology layers in CBDC implementation are:

Technology layer

Description

Core Blockchain Infrastructure Layer

The CBDC system relies on a blockchain infrastructure, including the underlying blockchain technology (public, private, or consortium) and the consensus mechanism for secure, transparent transactions.

Smart Contracts Layer

Smart contracts, deployed on the blockchain, automate processes like settlement, compliance, and asset issuance in CBDCs. They enforce predefined rules, reducing manual errors.

Digital Identity and Authentication Layer

CBDCs need a strong digital identity solution for secure user verification and authentication. This layer employs cryptographic mechanisms to restrict system access to authorized entities.

Privacy and Security Layer

This layer secures transaction data and user information with encryption, key management, and access controls, preventing unauthorized access and cyberattacks.

Tokenization and Asset Management Layer

CBDCs tokenize traditional assets, managing token creation, issuance, and tracking for assets like fiat, bonds, or commodities, ensuring accurate ownership records.

Interoperability and Integration Layer

This layer enables CBDC system interoperability with existing financial infrastructure through protocols, APIs, and standards, facilitating seamless interaction with payment systems and financial institutions.

User Interface and Experience Layer

The user interface layer offers front-end applications like mobile apps, digital wallets, and online platforms for users to manage CBDC holdings, initiate transactions, and monitor accounts.

Regulatory Compliance and Reporting Layer

This layer ensures CBDC systems comply with AML and KYC regulations, ensuring transaction and user data adhere to legal frameworks and support accurate reporting.

These technology layers must work in harmony to create a comprehensive and functional CBDC ecosystem. While the initial success of the ecosystem lies in successful implementation of MVP, usability, scalability and system integrity are key factors that create trust within the ecosystem.

CBDC challenges for Quality Engineering teams

The immutable nature of blockchain technology means that Quality Engineering plays a key role in successful implementation and adoption. It is important to consider and build a comprehensive strategy that would take the following into consideration. Quality Engineering teams face specific challenges in the implementation of CBDCs due to the unique characteristics of this digital financial ecosystem.

Quality Engineering challenges specific to CBDC implementation include:

Complex Ecosystem Testing: CBDC systems comprise interconnected components like blockchain infrastructure, smart contracts, user interfaces, and authentication systems. Quality engineers test the entire ecosystem for seamless integration and functionality.

Decentralized Nature: CBDCs often run on decentralized blockchains, necessitating testing with simulated network conditions, nodes, and consensus mechanisms to ensure consistent distributed network performance.

Smart Contract Verification: Smart contracts play a significant role in CBDC operations. Quality engineers must thoroughly review, test, and audit these contracts to identify vulnerabilities and ensure their accuracy and security.

Data Privacy and Security: CBDCs involve sensitive financial data. Ensuring data privacy and security while maintaining transparency within the blockchain poses a challenge. Quality engineers need to design testing scenarios that validate data protection mechanisms without compromising blockchain transparency.

Regulatory Compliance: CBDCs must adhere to various financial regulations and compliance standards. Quality engineers need to ensure that the system enforces regulatory requirements while maintaining its efficiency and functionality.

Cross-Border Transactions: If CBDCs facilitate cross-border transactions, quality engineers must validate the interoperability of different CBDC systems, currencies, and regulatory requirements.

Scalability: CBDC systems need to handle a large volume of transactions efficiently. Quality engineers must conduct load testing to assess the system’s performance, scalability, and response times under different transaction loads.

Resilience and Fault Tolerance: Quality engineers need to design tests that evaluate the CBDC system’s ability to withstand technical failures, network disruptions, and cyberattacks while ensuring uninterrupted service.

User Experience: The user interface and experience play a crucial role in CBDC adoption. Quality engineers must ensure that user interfaces are intuitive, user-friendly, and accessible across various devices and platforms.

Smart Contract Upgradability: As CBDC systems evolve, smart contracts may need to be upgraded or modified. Quality engineers must ensure that these updates are thoroughly tested and do not introduce vulnerabilities or conflicts.

Conclusion

Addressing these challenges requires a holistic approach to Quality Engineering, including collaboration with developers, security experts, regulatory professionals, and other stakeholders. By rigorously testing every aspect of the CBDC system and ensuring its compliance with industry standards, quality engineers play a crucial role in building a trustworthy and efficient digital currency ecosystem.

At Qualitest, we’ve partnered with clients on digital asset implementation projects. Our defined test strategies cover the full lifecycle of digital assets. Our dedicated Blockchain Center of Excellence conducts research into the latest developments in Web3, Digital Assets, DeFi, Blockchain, Distributed Ledgers, and we develop Quality Engineering solutions that respond and add value to our clients.